One of the narratives being pushed by Russia is that its economy is doing better than the West, and that sanctions are not working. This column looks at how the Russian economy worked before the invasion in 2022 and some of key statistics currently coming out from Russian authorities. The findings suggest that the Russian economy is not strong. Fiscal stimulus is creating inflation rather than growth, and the central bank is having to deal with the collateral damage of Russia’s aggression in Ukraine. More importantly, Ukraine’s Western partners have all the economic resources Ukraine needs to help it win the war.

Director Stockholm Institute of Transition Economics

Russian propaganda, with its false narratives, aims to affect all discussion related to its aggressive war in Ukraine, including the support the West provides to Ukraine and the impact sanctions have on the Russian war machine. One of the narratives produced by Russia tries to convince the West that there is no hope for Ukraine since the economy that is the basis of the Russian war machine is too strong and not affected by sanctions. 1

However, wars are determined by the relative strengths of the attacker and defender. If Ukraine were to defend its citizens and territory without external support, this would be an uphill battle to say the least. Russia’s economy pre-2022 was around ten times the size of the Ukrainian economy. However, Ukraine has a large share of the democratic world on its side in this war and their economies are 25 times the size of the Russian economy.

Furthermore, the Russian economy has significant weaknesses in its dependency on energy exports and the need to import many high-tech and other components that go into producing the arms it uses to attack Ukraine. This is well-known to the rest of the world and therefore both energy exports from Russia and exports of many goods to Russia have been put under sanctions by Ukraine’s partners in the West. Nevertheless, the Russian narrative continues to try to convince its internal and external audiences that the economy is doing better than the West, and that sanctions are not working.

Against this backdrop, the Stockholm Institute of Transition Economics (SITE) at the Stockholm School of Economics, published a report on The Russian Economy in the Fog of War (SITE 2024). The aim of the report is to document how the Russian economy worked before the full-scale invasion in 2022 and scrutinise some of the key statistics that are currently coming out as official statistics from Russian authorities. The first thing to note is that almost all economic analysis regarding any economy is based on official statistics. However, Russia today is not publishing all the normal statistics regarding its economy. This includes hiding important details regarding the government’s budget, trade, and financial transactions. At the same time, statistics on inflation and real GDP growth are published – two key macroeconomic indicators that are then widely cited by the media, international financial institutions (IFIs), and policymakers. Without much commentary around the credibility of these numbers or independent analysis of why these numbers are published. And in many cases used to make the argument that sanctions are not working and that the Russian war economy is doing well. All in line with Russian propaganda.

However, the SITE report shows that these key indicators are likely understating the true level of inflation and overstating real GDP growth (which is no small part depends on inflation). These conclusions are based on two important observations.

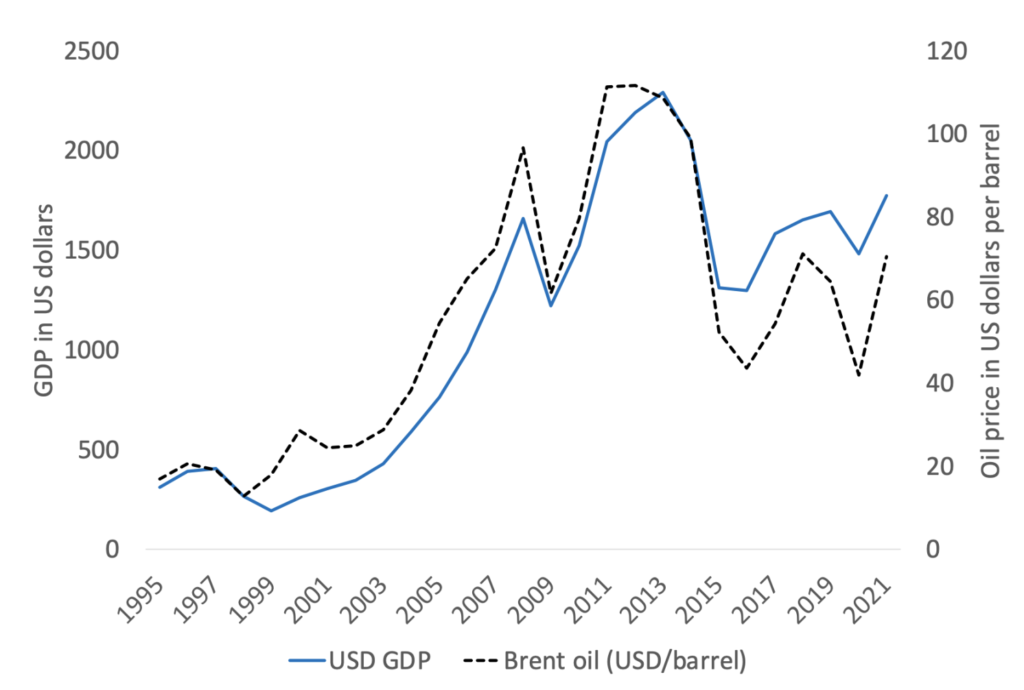

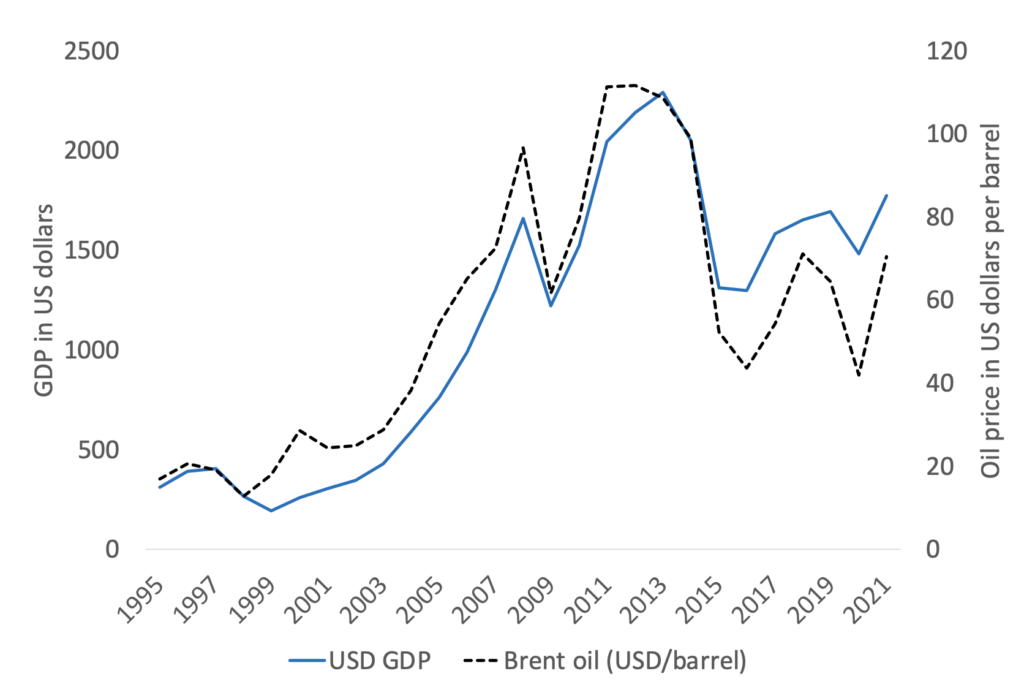

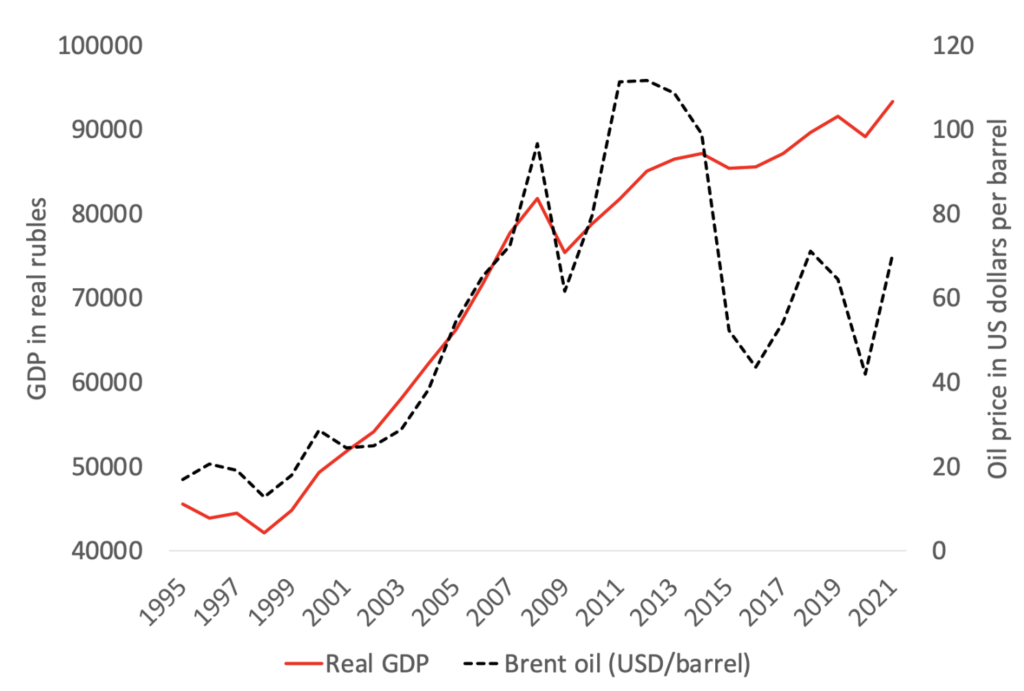

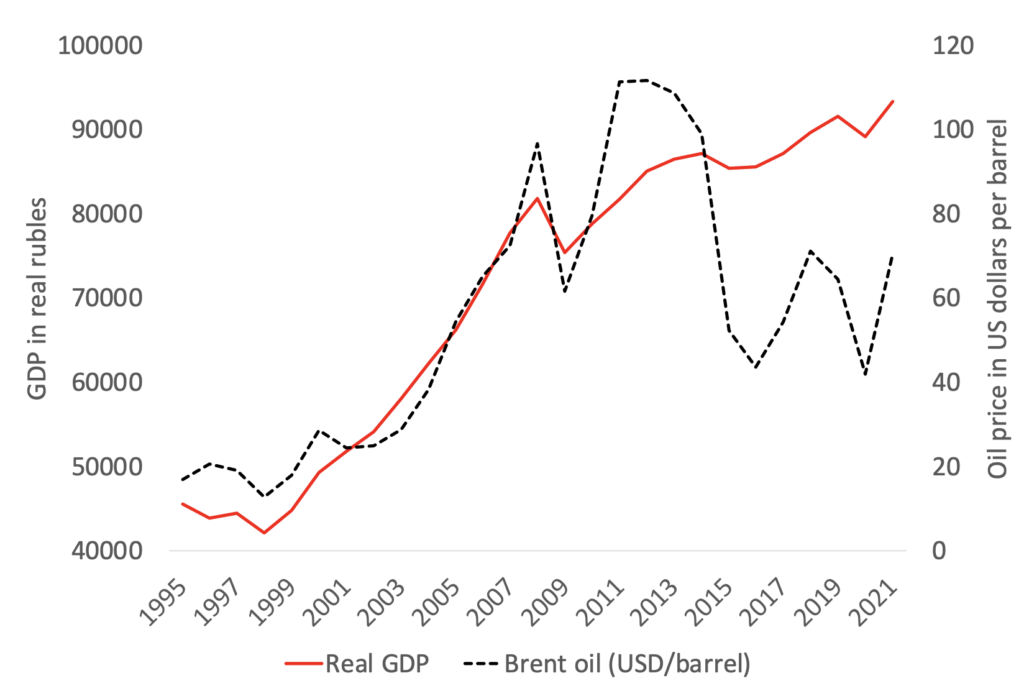

First, Russia’s real GDP growth has for the last 30 years been closely linked to the price Russia gets paid for the barrels of oil it exports. In a very simple growth regression, 60% to 90% of Russia’s GDP growth can be explained by one variable, namely, changes in oil prices (Becker 2016). The exact number depends on the time period and the measures we use for GDP. But in all versions of this basic macro model, changes in oil prices drive growth in Russia. Period.

Figure 1 Russian GDP and the price of oil

Source: Rosstat and U.S. Energy Information Administration

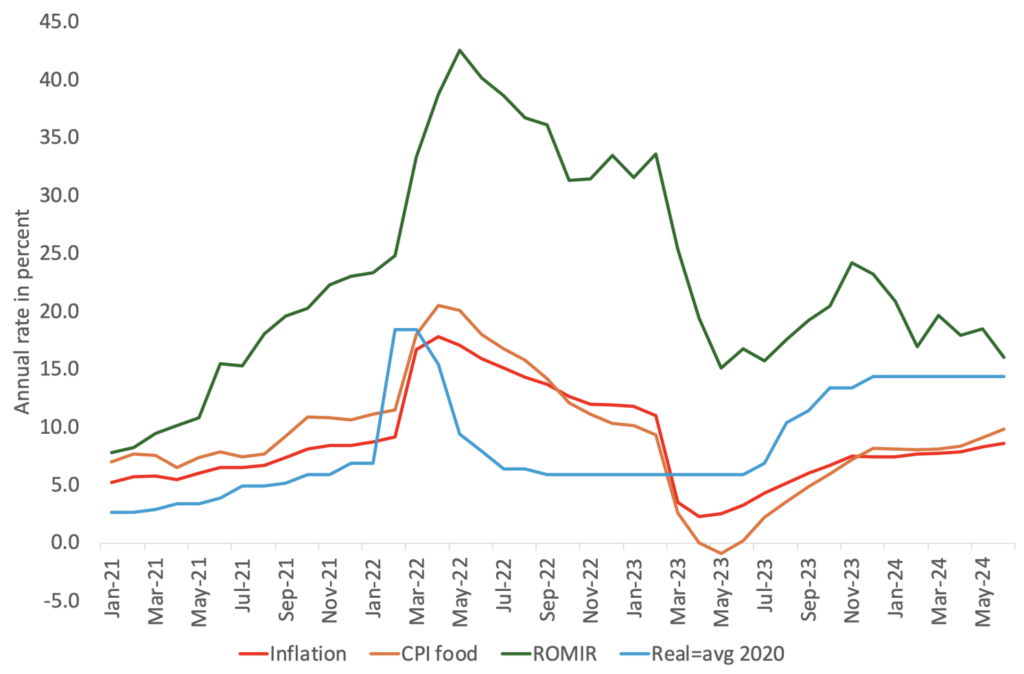

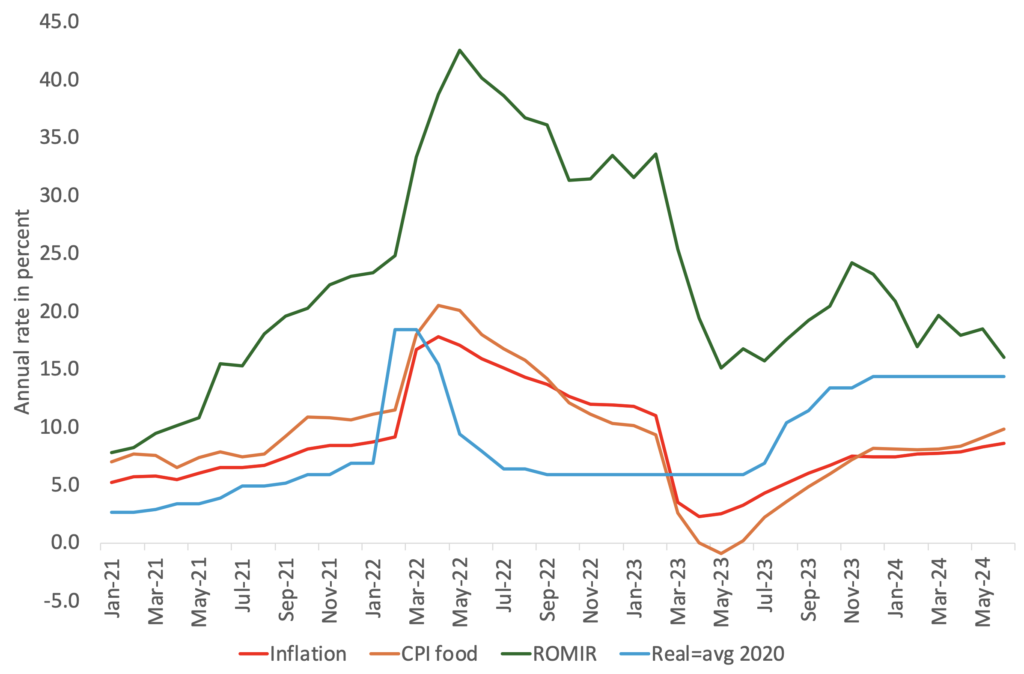

Second, inflation as measured by ROMIR, an independent data collector of inflation, shows that the official inflation numbers are vastly underestimated or underreported by official sources. Their inflation estimate is consistently at least twice as high as the official numbers. Furthermore, the actions taken by the Central Bank of Russia (CBR) regarding its key policy rate are another indication that inflation is significantly higher than what is officially reported. Most recently, the CBR hiked the policy rate to 21%(!) when inflation is still supposed to be in single digits (8.6% in September, the latest available number). This would imply a real interest rate in double digits, 12% percent or more. Not exactly consistent with the actions of other central banks around the world.

Figure 2 Alternative measures of inflation

Note: All series are monthly and show annual inflation based on the same month previous year.

Source: Rosstat, CBR, ROMIR, and authors’ calculations

In the report, we therefore note that more reasonable estimates of inflation are at least twice as high as official numbers. On top of that, the value of the ruble has depreciated significantly over the last two years, despite various regulations from the CBR that aim at keeping the ruble stronger.

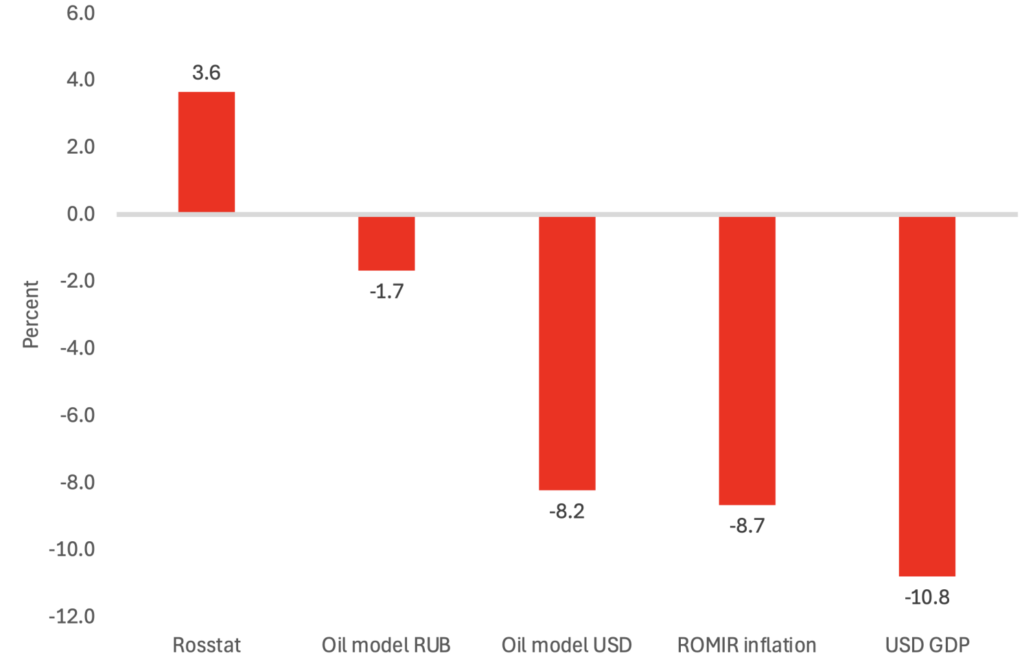

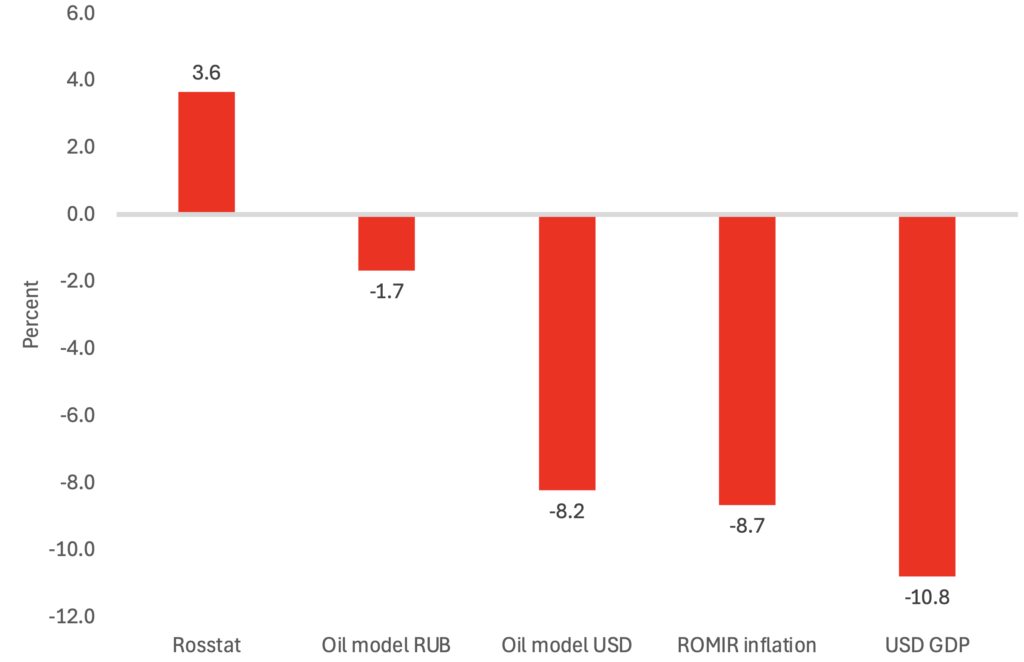

When we look at model predictions, alternative measures of inflation, and GDP measured in dollar terms in 2023, in turns out that all alternative measures of GDP growth in Russia are negative, ranging from minus 2% to minus 10%. This can be compared to the official real GDP growth in 2023 of plus 3.6%.

Figure 3 Alternative measures of GDP growth in 2023

Source: Rosstat, ROMIR, U.S. Energy Information Agency and authors’ calculations

The factor that is supposed to lead to this GDP growth is the fiscal stimulus the Russian government is providing by spending insane amounts of money on the war. However, this does not show up in their own breakdown of GDP in 2023 and, as all students of economics know, fiscal stimulus in an economy with supply constraints leads to inflation, not growth.

In short, the Russian economy is not strong. Fiscal stimulus is creating inflation rather than growth. And the CBR is now trying to deal with this collateral damage of Russia’s aggression in Ukraine. But more importantly, Ukraine’s Western partners have all the economic resources Ukraine needs to help it win the war. If the political will is there and we do not fall for a false Russian narrative regarding the relative strength of our economies, we can finance Ukraine’s victory. To the benefit of Ukraine most importantly but also to the benefit of current and future citizens of the entire democratic world.

Source: cepr.org